OTPP's Mid-Year 2017 Report?

The Ontario Teachers’ Pension Plan reached an asset total of $180.5 billion as of June 30, 2017, representing a $4.9-billion increase since the start of the year.Ontario Teachers' put out this press release going over mid-year results:

“Central banks are pulling liquidity and the geopolitical realities speak for themselves. While these factors lend uncertainty to markets, I’m pleased we had a half year with solid returns,” said chief executive officer Ron Mock during the plan’s mid-year conference call.

The plan’s net return was 3.6 per cent, equalling an investment income of $6.4 billion. “These results illustrate that we have remained disciplined and are executing against our strategy of investing for the long term,” said Mock.

Shifts in asset class exposure have been broadly positive for the fund. “As we balance our portfolio risk, we have increased our exposure to private asset classes while decreasing our exposure to public equities,” said Bjarne Graven Larsen, chief investment officer. “At the same time, we are leveraging our core active management strength across all asset classes. As such, we have reduced out allocation to passive equity investments and increased our allocation to actively managed investments.”

Inflation-sensitive assets were the only asset class that performed worse than anticipated given market conditions, said Larsen.

The Canadian dollar’s appreciation against many global currencies during the first half of the year was a significant factor to contend with. Gross asset return in local currencies was 4.5 per cent. “Currency volatility continues to be a theme in 2017, shaving 0.8 per cent from returns in the half of the year in Canadian dollar terms. This is because we invest in 37 currencies in over 50 countries but we report all assets and liability in Canadian dollars.”

“While we like foreign assets, we do not always like the associated currency risk.” The currency risk has held an evident sting in 2017 so far: in dollar terms, that 0.8 per cent meant $1.4 billion less in returns.

Ontario Teachers' Pension Plan (Ontario Teachers') today announced its net assets reached $180.5 billion as of June 30, 2017, a $4.9 billion increase from December 31, 2016. The total-fund gross return was 3.7% (3.6% net of investment administrative expenses), reflecting $6.4 billion of income generated by investments.You can also read OTPP's mid-year 2017 report here. It covers the mid-year results in more detail.

The five- and ten-year gross returns as at December 31, 2016 are 10.5% and 7.3% respectively. Since its inception in 1990, the Plan's annualized gross return as at December 31, 2016 was 10.1%.

"At Ontario Teachers' our investment portfolio is designed for stable performance in a variety of market conditions," said Ron Mock, President and Chief Executive Officer. "Our international team of investment professionals is focused on identifying opportunities to help deliver sustainable pensions to our members."

Ontario Teachers' continued to execute on its long-term strategy based on three pillars: total-fund returns, value-add (above benchmark) returns, and risk management. Key initiatives in this area include the launch of a department responsible for developing global investment relationships, and the centralization of trade and treasury functions to improve efficiency, support innovation and decrease execution costs.

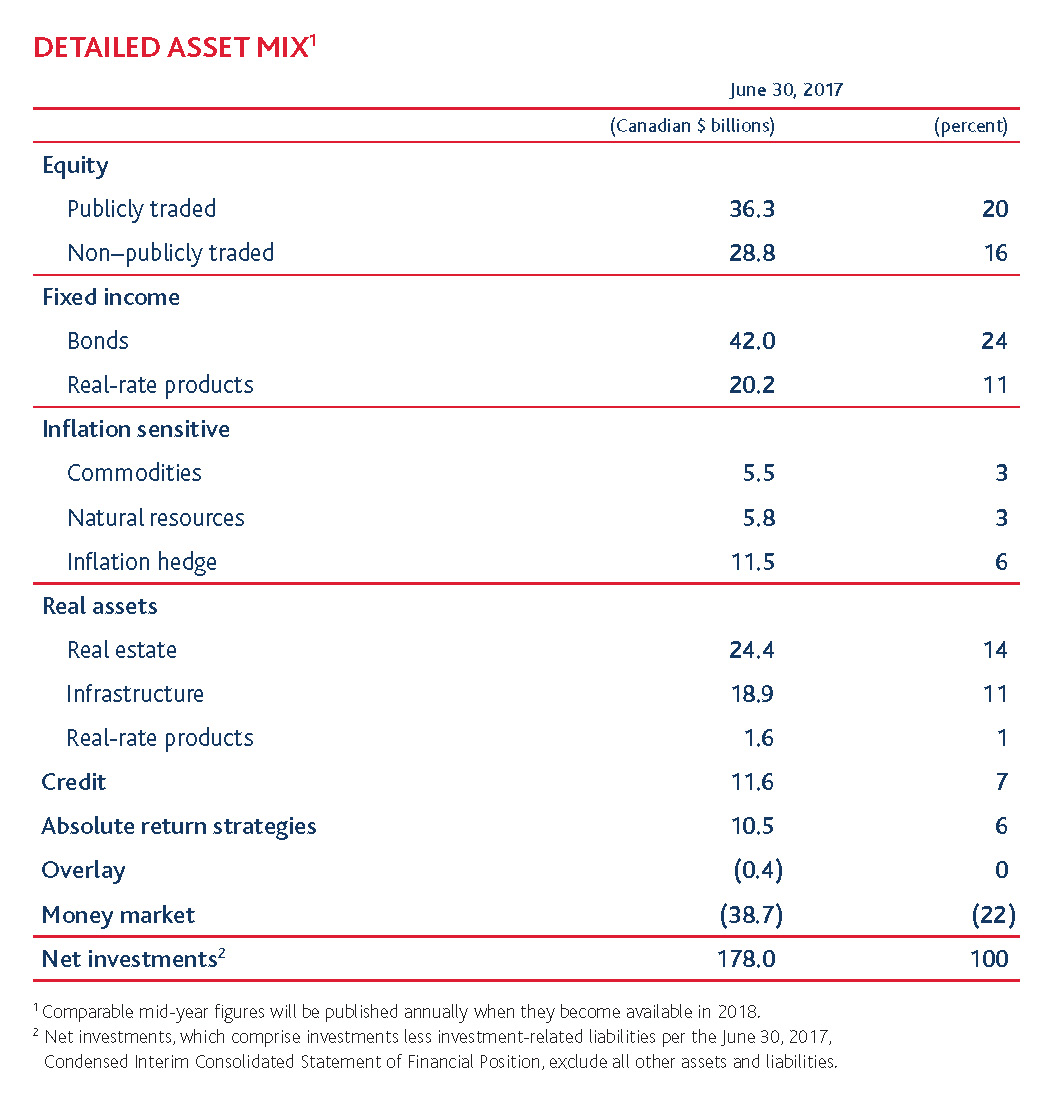

It also involved the implementation of Ontario Teachers' previously-announced asset class realignment to better reflect the behaviour and risk-profile of its investments, as follows (click on image):

"Returns in the first half of 2017 were driven by strong performance from global public equities, infrastructure, private equity and government bonds. Overall returns were offset by the impact of currency and declining commodity and natural resource prices," said Chief Investment Officer Bjarne Graven Larsen.

Ontario Teachers' takes a disciplined approach to managing the portfolio through a variety of different market conditions. A forward-looking and inclusive focus across the organization helps ensure a diverse allocation of risk with appropriate and aligned interest rate, inflation, foreign exchange and equity exposures.

Gross asset return in local currency was 4.5%. The Plan invests in 37 global currencies and in more than 50 countries, but reports its assets and liabilities in Canadian dollars. In the first half of 2017 the appreciation of the Canadian dollar had an impact of - 0.8%, or -$1.4 billion, on the Plan's total-fund gross return.

In June, as a result of the preliminary surplus reported as of January 1, 2017, the Ontario Teachers' Federation (OTF) and the Ontario government, which jointly sponsor the pension plan, announced they will use surplus funds to restore full inflation protection for retired members and decrease contribution rates by 1.1% for active members. Both changes are effective January 1, 2018.

*Net of trading costs, investment management expenses and external management fees, but before Ontario Teachers' investment administration expenses.

About Ontario Teachers'

The Ontario Teachers' Pension Plan (Ontario Teachers') is Canada's largest single-profession pension plan, with $180.5 billion in net assets at June 30, 2017. It holds a diverse global portfolio of assets, approximately 80% of which is managed in-house, and has earned an annualized gross rate of return of 10.1% since the Plan's founding in 1990. Ontario Teachers' is an independent organization headquartered in Toronto. Its Asia-Pacific region office is located in Hong Kong and its Europe, Middle East & Africa region office is in London. The defined-benefit plan, which is fully funded, invests and administers the pensions of the province of Ontario's 318,000 active and retired teachers. For more information, visit otpp.com and follow us on Twitter @OtppInfo.

Last month, I covered the Caisse and CPPIB's performance updates and stated the following:

[..] I typically don't cover CPPIB's quarterly results or la Caisse's mid-year results. In fact, I truly believe both organizations should abolish these intra-year performance updates, they are a nuisance and in my opinion, totally useless.Now, I still hold the view that large pensions should only report their results once a year but for some reason, mostly owing to transparency, we are seeing more and more large Canadian pensions report more frequently and give us mid-year or quarterly performance updates.

Why? Who cares how CPPIB performs in any given quarter or what la Caisse's mid-year results are? These pension funds manage billions in pension assets for people who have long-dated liabilities, so the only results that truly matter are long-term results.

The other reason why I don't cover these performance updates in detail is they typically omit valuations of private markets, I know that's a fact for CPPIB but maybe la Caisse includes them in their mid-year results.

Having said this, following the 2008 debacle, la Caisse has to report its mid-year results by law and so does CPPIB, its law says the Fund will provide quarterly updates of its performance.

[Note: In an email, OTPP's President and CEO, Ron Mock, shared this with me on these mid-year updates: "Yes they are here to stay. We now have a commercial paper program. Market needs more frequent updates as other plans do. So it is something we will be doing as an ongoing semi annual process. Mid year and year end."]

Just like the Caisse and CPPIB, strong performance in global public equities really helped Ontario Teachers' in the first half of the year but since the plan doesn't hedge currency risk, the soaring loonie impacted its performance in Canadian dollars which is what the liabilities are calculated in.

Let me show you a one year chart of the CurrencyShares Canadian Dollar Trust (FXC):

Notice how since touching a low of 71.70 in early May, it has surged to 81.21 in a little over three months. The loonie has really been on a tear in the last few months. This will undoubtedly impact the second half results of these large Canadian pensions that don't hedge currency risk.

You might be wondering what is driving this surge in our Canadian currency. Oil prices are lingering between $45 and $50 a barrel, the Canadian economy is suffering from huge debt issues and as I stated in my last comment which quickly got propelled to the most popular comment I've written in a very long time, the Bank of Canada is flirting with disaster, raising rates at a time when the global deflation hurricane is about to hit our most important trading partner.

No doubt, raising rates attracts foreign investors looking for yield and a "safe haven" currency but the reality is the fundamentals in Canada don't justify such an appreciation of our currency.

Just by looking at the chart, I can tell you short sellers covered their short positions as CTAs continued their buying program, buying the loonie on every dip and squeezing short sellers to cover.

Will the loonie hit parity again? I strongly doubt it unless oil goes back over $100 a barrel but this is a perfect example of how markets can stay irrational longer than you can stay solvent.

Anyway, these type of huge currency swings in the Canadian dollar really impact Canada's large pensions which don't hedge their currency risk.

In effect, by not hedging currency risk, they are long US dollars and other currencies like the yen and euro over the long run, but mostly US dollars since a huge chunk of their public and private assets are in the United States.

Importantly, not hedging currency risk leaves these large funds exposed when the loonie soars to new highs, but it also allows them to gain extra and often significant currency gains when the loonie plunges to new lows.

Over the very long run, I agree with the decision not to hedge currency risk because I too am naturally long US assets over the long run, even if that means sustaining losses in my personal account when the Canadian dollar rallies like it has since the beginning of the year.

But some large Canadian funds do partially or fully hedge currency risk. For example, I know for a fact that HOOPP fully hedges its currency risk because its CEO, Jim Keohane, once explained to me that since they match assets and liabilities very closely, they want to pay for the protection to hedge currency risk.

It makes sense but it leaves HOOPP exposed in years when the Canadian dollar plunges or underperforms major currencies, in particular the USD. HOOPP is a bit of an outlier, in the sense that is super funded and doesn't have the global exposure across public and private markets that its larger peers have, so it can afford to fully hedge currency risk.

I believe if HOOPP was as big as OTPP or CPPIB, it would necessarily be adopting many of the strategies these two funds have adopted, namely, more reliance on external managers in public and especially private markets and it would decide not to hedge currency risk.

However, what HOOPP and Ontario Teachers' do have in common is their internal operations and ability to manage assets internally across many platforms, including absolute return and private market strategies. This helps lower overall costs significantly.

The other thing they have in common is they both have a large exposure to bonds and they're both fully-funded (OTPP) or super funded (HOOPP).

What this means is they can afford to restore full inflation protection (OTPP) and/ or cut the contribution rate of their plan sponsors or in the case of HOOPP, increase benefits even more than just by restoring full inflation protection.

I have mixed feelings about this passage in Ontario Teachers' press release:

In June, as a result of the preliminary surplus reported as of January 1, 2017, the Ontario Teachers' Federation (OTF) and the Ontario government, which jointly sponsor the pension plan, announced they will use surplus funds to restore full inflation protection for retired members and decrease contribution rates by 1.1% for active members. Both changes are effective January 1, 2018.Don't get me wrong, it's great for Ontario's working and retired teachers and for the Ontario government, but I think this was a premature and very shortsighted move, one they will end up reversing over the next three years as the pension storm cometh, hitting all pensions, including OTPP and HOOPP.

This is a very important point I need to make, no matter how great Ron Mock and his team or Jim Keohane and his team are in terms of investing over the long term, they don't walk on water, and they cannot just invest their way into fully-funded status if a serious shock hits the global economy and global markets.

This is why they're jointly sponsored plans which have rightly embraced a shared-risk model which essentially means, if their plans hit a deficit in the future, some form of risk-sharing must take place among their respective plan sponsors, and that typically means cuts in benefits (typically partial or full removal of cost-of-living adjustments) or increases in contribution rate or both.

If I was advising the Ontario Teachers' Federation and the Ontario Government, I would unequivocally have told them to stay the course over the next three years and change nothing now that the plan is fully funded (save for a rainy day because a major shock is on its way).

It wouldn't make me popular but I'm not the type of person who is trying to win a popularity contest. I tell it like it is and if people don't want to face reality, they can deal with the consequences later.

Below, Ontario Teachers' CEO Ron Mock spoke at the Bloomberg Investment Summit earlier this year on Ontario Teachers' strategy for investing and attracting top talent. Listen carefully to this interview to fully understand why Ontario Teachers' and other large Canadian pensions are leaving their global peers in the dust when it comes to properly managing pension assets and liabilties.

Comments

Post a Comment